International Financial Reporting Standards (IFRS) 17 Insurance Contracts, issued in 2017, represents a major overhaul on financial reporting for insurance companies. However, many in the financial industry are still unfamiliar with the Standards. This blog post, Part 1, aims to answer the five basic W questions Who, What, When, Where, and Why of IFRS 17. The H, or How, will be discussed in Part 2.

Who issued IFRS 17?

IFRS 17 is issued by the International Accounting Standards Board (IASB). The IASB specifies how companies must maintain and report their accounts.

What is IFRS 17?

IFRS 17 is the accounting Standard for insurance contracts. The IFRS are designed to bring consistency, transparency, and comparability within financial statements across various global industries, and IFRS 17 applies this approach to the insurance business.

When is the effective date?

Initially set for January 1, 2021, industry leaders have requested to delay the effective date due to the amount of effort required to implement the new Standard alongside IFRS 9. Additionally, in March 2020 the COVID-19 pandemic influenced the IASB to defer the final effective date for IFRS 17 to January 1, 2023.

Where does IFRS 17 apply?

IFRS 17 applies to all insurance companies using the IFRS Standards. Currently, it has been estimated that 450 insurance companies worldwide will be affected. Insurance companies in Japan and the United States, however, use Generally Accepted Accounting Principles (GAAP)—a rules-based approach that is rigorous compared to the principle-based approach of IFRS. Therefore, IFRS 17 does not directly impact Japan or the U.S., but it could affect related multinational companies with insurance business overseas.

Why was IFRS 17 developed?

This section discusses some of the main issues with the current reporting standards (IFRS 4) which has led to the issuance of IFRS 17. They include inconsistent accounting, little transparency, and lack of comparability (see Figure 1).

Figure 1: Some of the main issues with IFRS 4.[1]

Inconsistent Accounting

IFRS 17 was developed to replace IFRS 4, which was an interim Standard meant to limit changes to existing insurance accounting practices. As IFRS 4 did not provide detailed guidelines, there were many questions left unanswered about the expectations for insurers:

- Are they required to discount their cash flows?

- What discount rates should they use?

- Do they amortize the incurred costs or expense them immediately?

- Are they required to consider the time value of money when measuring the liabilities?

Hence, insurers came up with different practices to measure their insurance products.

Little Transparency

Analyzing financial statements has been difficult as some insurers do not provide complete information about the sources of profit recognized from insurance contracts. For example, some companies immediately recognize premiums received as revenue. There are also companies that do not separate the investment income from investment-linked contracts when measuring insurance contract liabilities. As a result, regulators cannot determine if the company is generating profit by providing insurance services or by benefiting from good investments.

Lack of Comparability

Some multinational companies consolidate their subsidiaries using different accounting policies, even for the same type of insurance contracts written in different countries. This makes it challenging for investors to compare the financial statements across different industries to evaluate investments.

How does IFRS 17 replace IFRS 4?

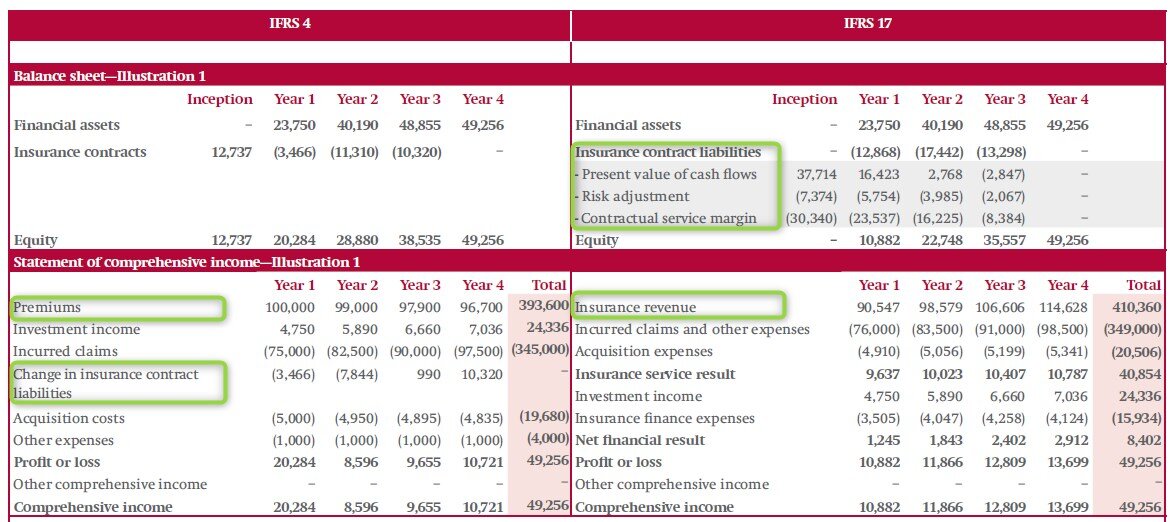

IFRS 17 introduces a standard model to measure insurance contract liabilities, changes the way insurers recognize profit (Insurance Revenue), and revamps the presentation of financial statements (see Figure 2). We will dive into these topics in Part 2 of this blog series.

Figure 2: A comparison of IFRS 4 and IFRS 17.[2]

[1] Appendix B – Illustrations, IFRS 17 Effects Analysis by the IFRS Foundation (page 118).

[2] Appendix B – Illustrations, IFRS 17 Effects Analysis by the IFRS Foundation (page 118).

Carmen Loh is a Risk Consultant with FRG. She graduated with her Actuarial Science degree in 2016 from Heriot-Watt University before joining FRG. She is currently the subject matter expert on an IFRS 17 implementation project for a general insurance company in the APAC region.